Mexico Beach to Cape San Blas 2022 Market Recap and looking to 2023

2022 was the 18th and wildest year that I’ve sold real estate from Mexico Beach to Cape San Blas. The beginning of the year and into spring was downright nutty with a frenzy of buyers, inventory extremely low, and prices flying up. The spring market here had purchasers buying whatever they could find and so few listings that most sales ended up in bidding wars. Comps didn’t matter and your offer wasn’t considered by many sellers if you wanted an appraisal. We were down to a historically low average of 13 homes on the market all the way from Cape San Blas to Indian Pass and only 28 available from Mexico Beach to WindMark Beach. Average 30 year mortgage rates were around 3.5%, and we witnessed the most rapid price increases seen since the 2004-2005 market.

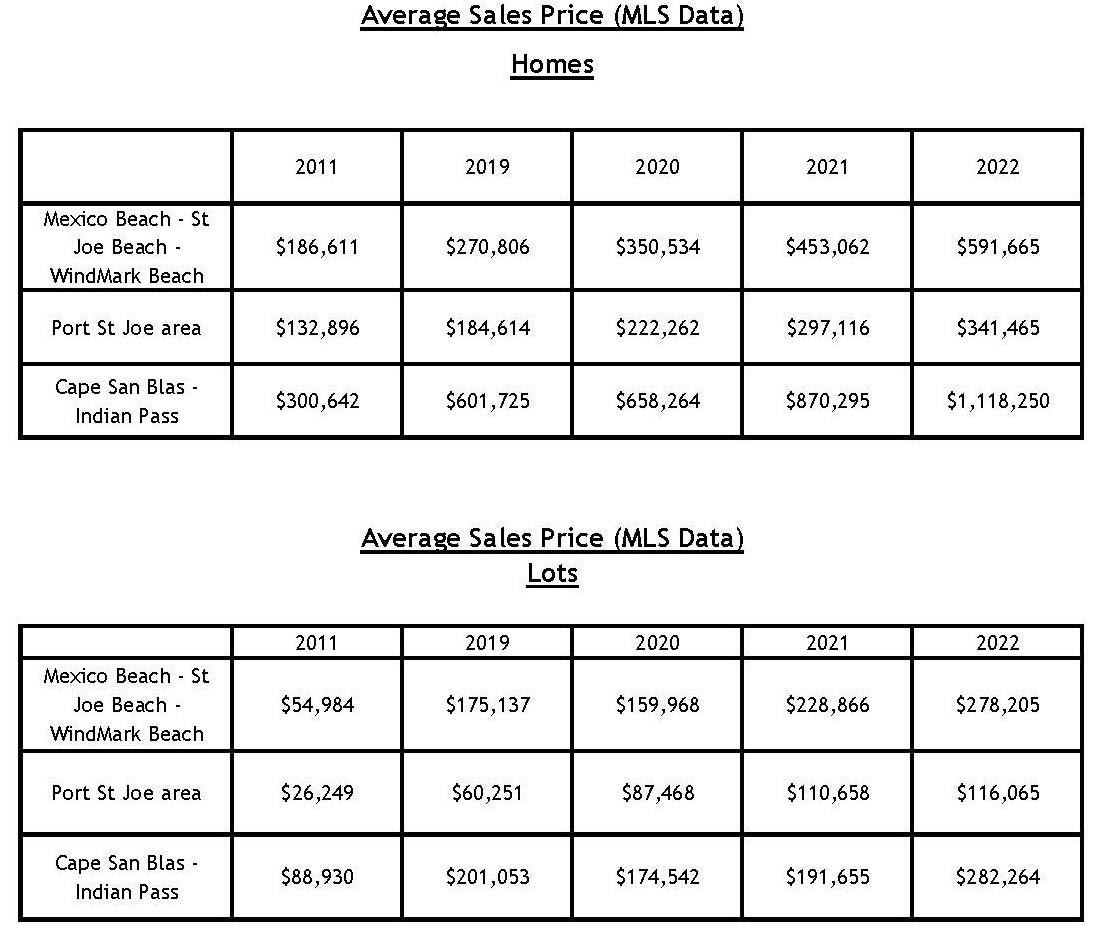

Interest rate increases, recession worries, and the war in Ukraine began to slow things in late spring. The market has far from stopped and have been able to hold on to most or all of its gains. 2022 will go down as a fabulous year in real estate with huge increases followed by slight decreases in some categories in the 2nd half of the year. If you own an average property in this area, your property is probably worth much more than it was 2021, but less than it could have brought in spring or early summer of 2022. It’s been one heck of an overall market with the average home doubling in value since 2019 and tripling since bottoming out near 2011. Vacant land has done almost as well and even better in some areas.

The market has definitely shifted from an extreme seller’s market to a market that now has more sellers than active buyers. The markets I’m seeing soften the most are 2nd home purchases, and there aren’t many people financing vacant land at current rates. Investment home buyers are only buying when the numbers make sense vs hoping for continued rent increases. Primary home markets are the strongest segment. There’s a large number of potential 2nd home/vacant lot buyers that have pushed the pause button hoping/thinking that either or both interest rates and/or prices will come down in ’23. Buyers a year ago felt they had to buy or prices would be higher the next month if they didn’t act quickly. Today many buyers aren’t confident in the market and are worried prices may fall. When you combine fewer buyers and more sellers that see the market/economy softening, the number of properties on the market starts to rise. The total number of homes on the market from Mexico Beach to Cape San Blas has increased from 70 in March to 195 today. Vacant lot inventory has increased from 123 in March to 200. Even though much higher than 9 months ago, these are not historically high or alarming numbers.

The market is usually slowest here in the winter and busiest in the spring and summer. 2022 was the first year in my career that demand peaked in spring and not summer. Sellers that tried for higher prices in summer than in the spring were most often left disappointed and either still own or made reductions. It was still an active summer, but the bidding wars had stopped and prices were holding, but not continuing to increase. Summer has the most people here and a percentage are looking to buy during their vacation which leads to summer usually seeing the most sales. I heard countless Realtors complaining about how “slow it was for summer.” In reality, I think we’d been spoiled for the previous year and a half. We ended with 533 sales in the first half of the year and 379 in the 2nd half; for 912 sales from MB to CSB. For comparison, there were 808 sales in 2019, 1030 in 2020, and 1328 in 2021. (All of these statistics are from the RAFGC MLS and there are additional sales like FSBO not included.) The demand and number of people wanting to move here full time is still solid. With all the negative economic news, the market is far from dead with 44 sales in December, and there are also 58 properties under contract as of today! These are pretty solid numbers, just not the craziness seen early last year. Cash buyers remained a dominant force in 2022 with 52% or 476 sales reported as cash purchases. Cash 1031 buyers facing tax deadlines made some of the high watermark sales for the year. Cash buyers haven’t gotten a discount in years with such a competitive market and are starting to once again become more desirable with discounts considered as we move into ’23.

I spend a great deal of time trying to figure out what the market will do moving forward. I’m curious about how others think the market will perform in 2023 and do a fair amount of reading online. The economists at the National Association of Realtors have the most bullish forecast from a group that I follow with a projected increase of 5.4% in 2023. Most other “experts” are projecting a slow and flat market or slight decreases. “Zillow expects national home values to remain relatively flat next year, and even fall in the most affordability-challenged markets.” Fannie Mae predicts a 1.5% decrease, Redfin predicts a decrease of 4%, and the largest predicted decrease nationally, I found with Morgan Stanley suggesting a 10% decrease in home values.

I’ve said for years and will say again: as long as the vacation rental market holds, I can’t see big decreases in home values. Enough owners count on this income to support their purchases that a substantial downturn in the rental market would be a big problem and start forcing sales. The best news I’ve heard for 2023 might be from talking to multiple rental management company owners. All have said their 2023 bookings are either up or at least in line with recent years. 2022 was a very good year for vacation rentals. For most owners/rental companies, it was either their best year ever or the 2nd best followed by 2021 when so many people were working from home and out of school due to Covid and vacationing during times that typically weren’t busy with vacationers. A couple of large vacation rental companies are telling me they are up considerably for Summer bookings compared to last year at this time, and I think that’s a great sign. I’ve heard positive news from owners that rent as well and some that were hoping to sell have already pulled off the market and are happy with renting until market conditions change back to a seller’s market.

A number of potential buyers believe there will be a considerable number of foreclosures. Most purchasers that purchased in years past can still sell for considerable profits or at least have equity which all but eliminates foreclosure risk. I read the national headlines about all the foreclosures that have started in the US, but we haven’t seen any signs of that locally. These same past purchasers that financed are also in on much lower mortgage rates than they could get today. This is leading to some sellers pulling off the market that were hoping to sell and then make another purchase. Our local area and Florida in general is also trending in a much more positive direction than many parts of the country for both full time residents and vacationers. I don’t think a flat market and slower market is necessarily a bad thing, even for investors when factoring in the huge gains in recent years. It will create a more balanced market vs the extreme seller’s market that existed in ’21 and early ’22. We’re trending towards buyers having some negotiating power and opportunities and still a moderate market for sellers willing to price competitively.

Market numbers suggest that the vacant land market is not as strong as the housing market, particularly in our beach areas. I agree with some outside investors watching our market that describe it as a bit of stalemate in recent months. The Mexico Beach to WindMark vacant land market is a good example with 86 properties for sale and only 3 purchases in December. That’s about 30 months worth of inventory compared to the frenzy in March where we averaged 32 lots on the market and 28 sales that month. Buyers are now wanting more of a discount than sellers will give. Many sellers are waiting on the typical large run of Spring buyers. I don’t think anybody will have a real idea of how 2023 is going to play out until we see how the Spring market plays out. If it remains slow, there will be some segments strained where sellers will have to reduce to sell. On the flip side, if spring is busy with buyers, we could see prices rising in the Summer as they do most years. What happens with interest rates will undoubtedly be a large factor.Mexico Beach to WindMark – Residential building and rebuilding remains strong with many new homes coming online. The day before Hurricane Michael, there were 1825 water accounts with the city and 2022 closed out with 1270 active accounts. Factoring in the apartments The St. Joe Company is building and homes under construction, this number should be at least over 1,500 by the end of 2023 with just what’s currently under construction. New commercial building and rebuilding since Michael remains much slower. We don’t have a new grocery store and only one sit down restaurant (Mango Marley’s) are the biggest complaints I hear. There’s also Shipwreck Raw Bar in St Joe Beach and The View and Bruno’s in WindMark. WindMark is growing leaps and bounds with DR Horton continuing to rapidly build homes for sale. 66 of the 125 homes mentioned below are Horton homes in WindMark, leaving a relatively low supply for St. Joe Beach and Mexico Beach. Zoning has become more flexible for food trucks, and there are 10 from St Joe Beach to Mexico Beach at this time. An Inland Sunstop Gas Station opened on the west end of Mexico Beach and is by far the largest and nicest in the area and an asset to the Mexico Beach community. Here’s the 125 homes and 86 lots for sale.

The rebuild of The El Governor Motel is coming along. Beach Planet, a retail beach shop, has recently received their building permit at the old 40th St Pizza location and we hope to see them start construction very soon. Bracewell’s Flooring and Fencing is building a new store in the old Civic Center location behind Mango’s. A restaurant group bought the building currently leased to Bracewell’s with plans to convert it into a restaurant projected to be open this summer. This group is also involved with rebuilding Toucan’s, which they hope to finally have a FDEP building permit this spring. I have seen the plans and they are awesome, unfortunately getting a permit like this for a project on the beach is very complicated. In regards to the pier, the city is still dealing with FEMA and their own FDEP issues. There’s no firm date to start construction of the pier, but the city is hopeful in can begin sometime in 2023.

Port St. Joe – The town of Port St Joe’s commercial development has been thriving. There have been many new business open in 2023. There is quite a restaurant scene with 20 open that are either on or within 1-2 blocks of Reid Ave. The town’s population is increasing and student numbers are back to pre-Michael numbers for the first time since 2018. Zoning limits vacation rentals, but it’s been a very popular market for full time buyers moving to the area. The rebuilt and larger Marina opened about a month ago and will be a huge asset missing since Hurricane Michael. There’s relatively low inventory for this segment with 34 homes and 27 lots for sale.

Cape San Blas Indian Pass – This area continues to grow in popularity for those looking to vacation in a laid back and uncrowded area. There’s not much commercial and that’s what most people love about it. A huge portion of new purchasers and renters are people tired of the 30A/Destin crowds and can also buy for a fraction of what homes cost in those areas. Rentals remain very strong throughout this area. The clear water and white sand of the North Cape far surpass any other submarket in prices with the average of 57 single family homes that sold reaching an eye popping $1,469,643. The slower pace of the South Cape and Indian Pass continue to also attract their own following for rentals and retirement/2nd homes. Here’s the 36 homes and 87 lots for sale.

North Gulf County / Wewa – I don’t try and cover this market as by far the top agent for this market year in and year out works with our office. This market remains much more affordable than the other markets in Gulf County or Mexico Beach with an average home selling for $167,965 in ’22. Miranda Rollins is who you need to speak with if interested in buying or selling in this market.

I’m very proud that 98 Real Estate Group finished for the 10th year in a row as the #1 producing real estate brokerage for the Mexico Beach to WindMark market. We’ve got over $100 million more in sales than our closest competitor in that time and I’ve been very blessed to be the broker of a great team of 19 agents and an amazing office manager. Life and my family are great while enjoying all of the local adventures outdoors and the joys of growing up in a small tight knit community.Cheers and Go Dawgs,

Zach Childs

Broker/Owner 98 Real Estate Group

#1 Producing Real Estate Company Located in Mexico Beach

2013, 2014, 2015, 2016, 2017, 2018, 2019, 2020, 2021 & 2022

Voted #1 Agent on The Forgotten Coast- 2013 and 2015

Cell: 850-819-0833

Fax: 888-382-9608

WWW.MEXICOBEACHSALES.COM

WWW.98RealEstateGroup.com